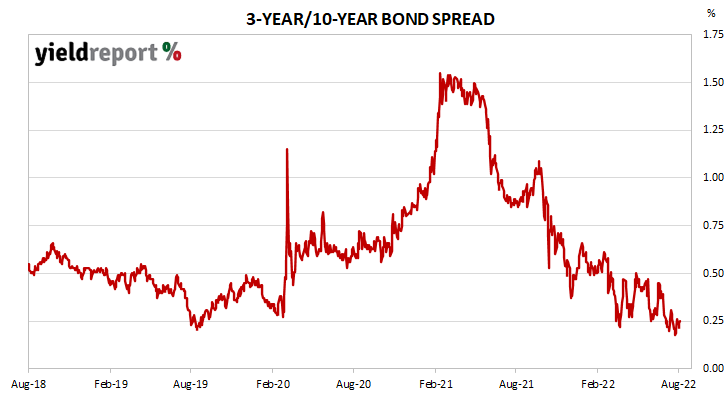

Summary: ACGB curve a touch flatter; US Treasury curve les negative/more positive.

The gradient of the ACGB yield curve became a touch flatter as the fall of shorter-term Australian yields were largely matched by the falls of their longer-term counterparts. By the end of the week, 3-year/10-year and 3/20 year spreads had both slipped 1bp to 25bps and 60bps respectively.

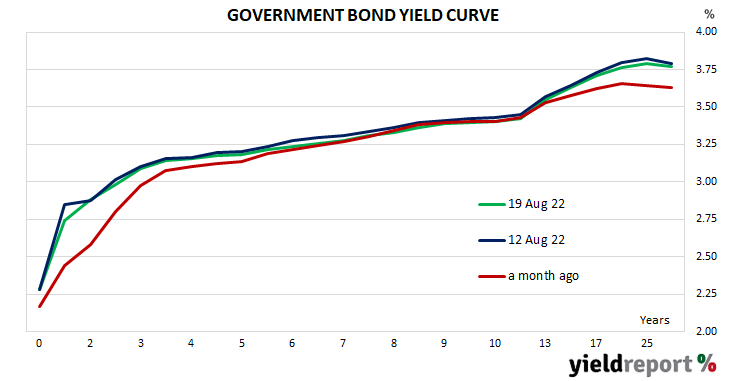

The various measures of the gradient of the US Treasury curve either became less negative or more positive. The 2-year/10-year spread gained 17bps to -25bps over the week while the 2 year/30 year spread added 13bps to -1bp. The San Francisco Fed’s favoured recession-predicting measure, the 3-month/10-year Treasury spread, finished 3bps wider at 31bps.

To find out more about the yield curve and its usefulness, click here or here.